Table of Contents

For the past two decades, Application-to-Person (A2P) messaging has been a key channel in business communications. Whether it’s authentication codes, transaction alerts, delivery updates, or promotional campaigns, A2P SMS has proven to be a trusted, scalable tool across industries and regions.

But despite its continued relevance, the wholesale messaging market is feeling the squeeze. While global demand for messaging remains strong, profit margins are declining, driven by rising operational costs, regulatory complexity, the increasing threat of fraud, and a shift toward alternative messaging channels. For telecom carriers, aggregators, and platform providers, the message is clear: strategic change is no longer optional, it’s necessary.

This article takes a close look at the key factors behind this margin compression, and how leading players in the industry are responding through smarter infrastructure, channel diversification, and operational efficiency.

A Market Under Pressure

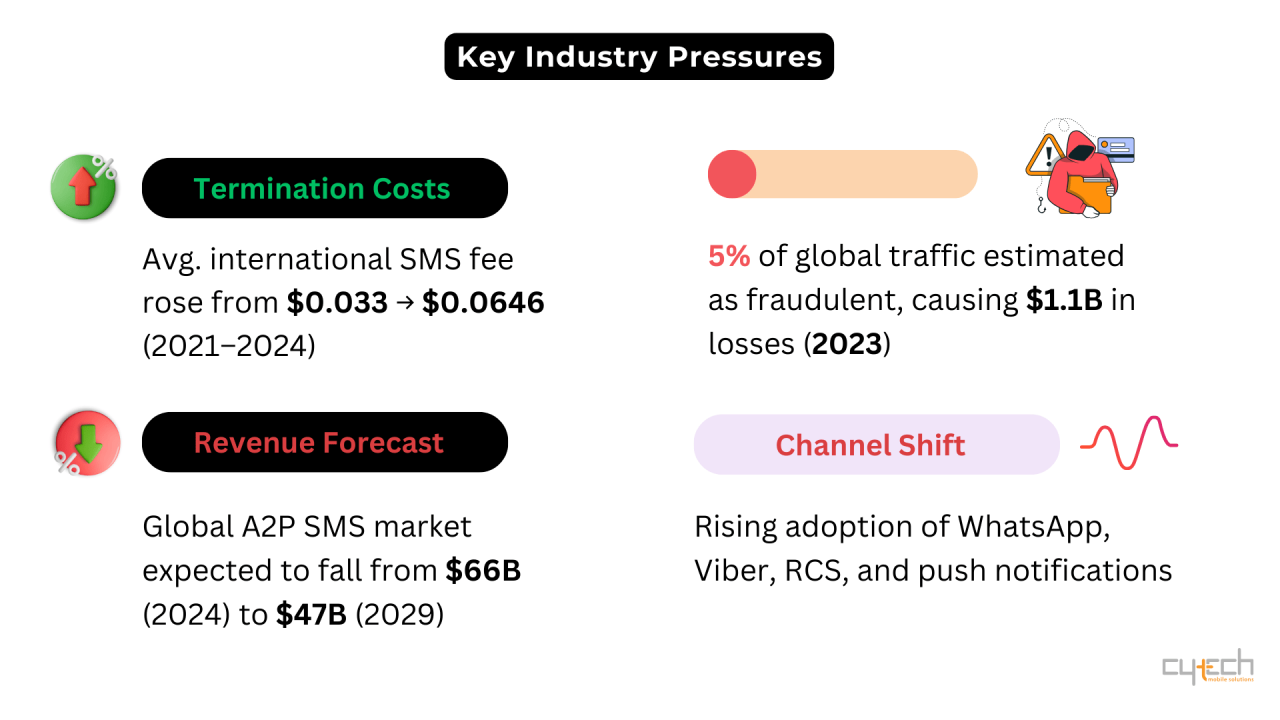

The global messaging industry is still vast, but its underlying model is under strain. Forecasts show that the global A2P SMS market, currently valued at approximately $66 billion (2024), is projected to shrink to $47 billion by 2029, a nearly 29% drop in just five years (Source).

One of the main reasons is cost. Between 2021 and 2024, the average international A2P SMS termination fee jumped from around $0.033 to $0.0646, almost doubling in three years (Source). Mobile operators raised prices to compensate for declines in peer-to-peer (P2P) messaging traffic, but this had a direct impact on the margins of intermediaries like aggregators and messaging platforms.

At the same time, fraud, particularly in the form of artificially inflated traffic (AIT) has surged. It’s estimated that in 2023, 5% of all global SMS traffic was fraudulent, leading to more than $1.1 billion in losses for the ecosystem (Source).

This combination of inflation, inefficiency, and fraud points to a key challenge for the sector: how to maintain profitability in an increasingly high-volume, low-margin business.

What’s Driving Margins Down?

1. Rising Termination Fees

Across the globe, mobile operators have raised SMS termination rates. In many cases, these fees have more than doubled within a short timeframe. These cost increases are typically passed down the chain, squeezing the margins of providers who are unable to raise prices at the same rate.

2. Market Saturation and Price Competition

In many regions, A2P messaging has reached maturity. Growth in message volume is slowing, while competition among CPaaS vendors and aggregators is intensifying. Price remains a major differentiator, driving many providers into a volume-first model that puts further strain on profit margins.

3. Regulatory Complexity

Compliance requirements, such as 10DLC registration in the U.S. or Sender ID frameworks in Europe and Asia, require significant administrative effort and incur additional fees. These frameworks are essential for trust and transparency but also add friction and cost for providers.

4. Fraud and Revenue Leakage

Practices such as SIM box usage, grey routing, and AIT are eroding revenues. Fraudulent messages often incur termination fees but provide no legitimate return. This not only causes direct financial damage but also undermines trust with enterprise clients.

5. The Rise of Alternative Channels

Businesses are increasingly turning to platforms like WhatsApp Business, Viber, RCS, and push notifications. SMS remains critical, but it’s no longer the only channel in play. Clients are demanding multichannel solutions that better align with customer behavior, and that puts pressure on SMS-dominated models.

How the Industry Is Responding

While the environment is challenging, the response from the industry has been strategic. Rather than retreat, many providers are pivoting—adopting smarter models and investing in more sustainable infrastructure.

1. Expanding to Omnichannel Services

Leading platforms are no longer SMS-only. Providers are now integrating a range of communication tools, WhatsApp, RCS, email, push notifications to support different business needs. This channel flexibility not only improves effectiveness but also opens up new revenue streams with better margin potential.

2. Embracing CPaaS

The move toward Communications Platform as a Service (CPaaS) is reshaping the market. Instead of simply delivering messages, providers now offer full platforms with APIs, orchestration tools, analytics, and integrations with enterprise systems. These value-added services offer stickier relationships and higher revenue per customer.

3. Investing in Security and Fraud Prevention

Fraud detection and prevention is no longer a “nice to have” it’s a core requirement. Companies are investing in real-time monitoring tools, SMS firewalls, and AI-based anomaly detection to prevent traffic abuse. These investments reduce leakage, improve network quality, and help rebuild enterprise trust.

4. Operational Optimization

Efficiency is now critical. Providers are reducing costs by implementing least-cost routing (LCR), automating processes, and migrating infrastructure to the cloud. These steps offer better agility and scalability, ensuring that operations stay lean even as the landscape evolves.

Market Overview: 2023–2024 Snapshot

| Key Indicator | Current Trend |

|---|---|

| Average A2P SMS Termination Fee | Increased from $0.033 (2021) to $0.0646 (2024) |

| A2P SMS Revenue Forecast | Declining from $66B (2024) to $47B (2029) |

| Share of Fraudulent SMS Traffic | Estimated at 5% globally |

| Financial Impact of SMS Fraud | Over $1.1 billion in lost revenue (2023) |

| CPaaS Revenue Growth | Expected to rise from $3.4B (2023) to over $10B (2028) |

| Enterprise Adoption of OTT Channels | Rapidly increasing for richer, more interactive messaging |

Looking Ahead: More Complexity, But Also More Opportunity

The decline in margins is part of a larger shift in how enterprises communicate. The era of SMS-only strategies is fading. What’s emerging is a more integrated, intelligence-driven approach, built around omnichannel communication, data visibility, and security.

Success in the coming years will depend not on message volume alone, but on the ability to:

- Offer the right channel mix for different customer needs,

- Optimize delivery paths and routing in real time,

- Protect infrastructure from fraudulent traffic,

- Provide scalable, feature-rich platforms that enable automation and insight.

Conclusion

Wholesale messaging is undergoing structural transformation. A2P SMS remains valuable, but the economics around it are evolving. Providers that adapt, by diversifying their offering, securing their networks, and delivering richer platform capabilities, will not only survive but lead. As enterprise clients continue to demand reliable, secure, and cost-effective communication solutions, the real opportunity lies not in holding on to legacy models, but in building the next generation of messaging services.

")