Table of Contents

The wholesale Application-to-Person (A2P) SMS market is undergoing a structural transformation. For over a decade, business messaging operated on a volume-driven model: brands sought cheap bulk rates, aggregators optimized routing, and Mobile Network Operators (MNOs) acted as passive message carriers. Today, the rapid rise of bypass fraud, grey routing, and artificial traffic has forced a fundamental reset. At the center of this shift is the next-generation SMS firewall. Once viewed strictly as security hardware, the modern firewall has evolved into an active monetization engine. By redefining traffic classification, blocking, and billing, firewall monetization is rewriting wholesale messaging economics, shifting the ecosystem from low-margin volume to highly managed, value-oriented structures.

The High Cost of Leakage and the Monetization Shift

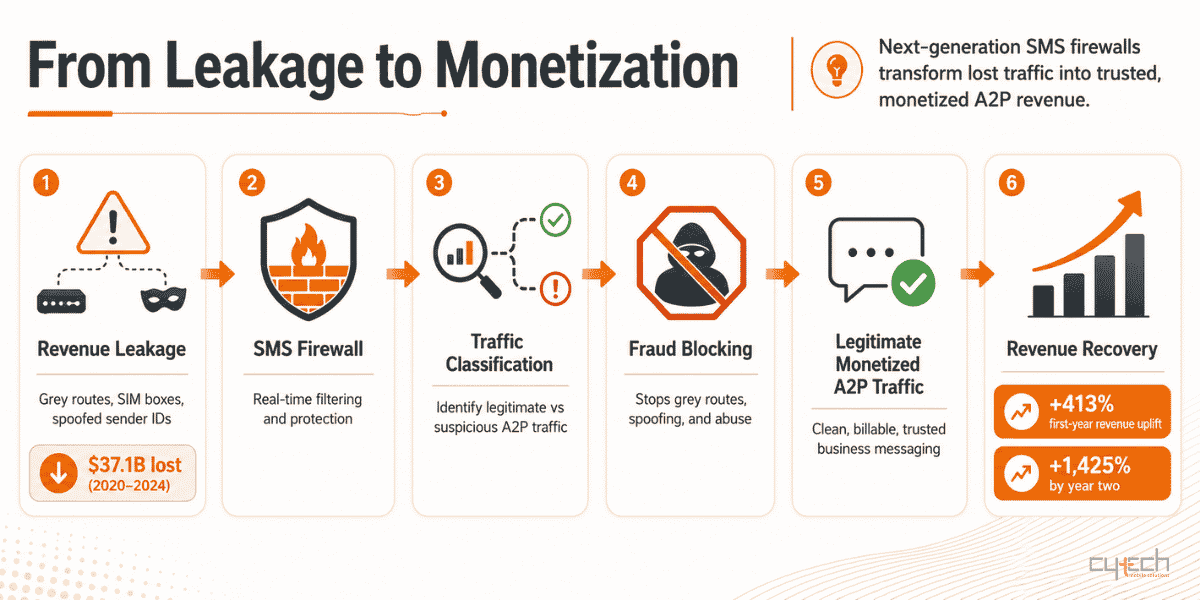

Historically, MNOs suffered massive revenue leakage due to grey routes—unauthorized pathways, such as SIM boxes and interconnect abuse, that bypass commercial termination agreements. Between 2020 and 2024, grey routes and A2P fraud cost MNOs a cumulative $37.1 billion, representing an annual average leakage of $7.69 billion. To recapture this lost revenue, operators are deploying next-generation SMS firewalls capable of real-time deep packet analysis, spoofed sender ID protection, and grey route blocking.

The financial impact of this transition is immediate. MNOs deploying advanced firewalls frequently experience a dramatic surge in legitimate, monetized traffic. Operators implementing managed firewall solutions see an average immediate uplift in A2P SMS revenue of 413% in the first year, rising to 1,425% by the second year. This has triggered a global investment wave, with the SMS firewall market projected to grow from $2.56 billion in 2024 to $9.2 billion by 2035.

To stabilize these streams, some operators are migrating from traditional volume-based termination to subscriber-based A2P monetization models. This subscriber-centric approach transforms existing number inventories into predictable, recurring revenue streams without requiring heavy upfront capital expenditure (CAPEX), as modern firewall platforms are increasingly deployed via cloud or managed-service models.

| Monetization Model | Charging Mechanism | Core Advantage for MNOs |

|---|---|---|

| Volume-Based | Per-message international termination rate (ITR) | High revenue potential during peak traffic periods |

| Subscriber-Based | Fixed monthly fee per active network subscriber | Predictable, recurring revenue; eliminates volume volatility |

| Hosted / Managed | Revenue-share model with zero upfront CAPEX | Immediate deployment; externalizes post-launch tuning costs |

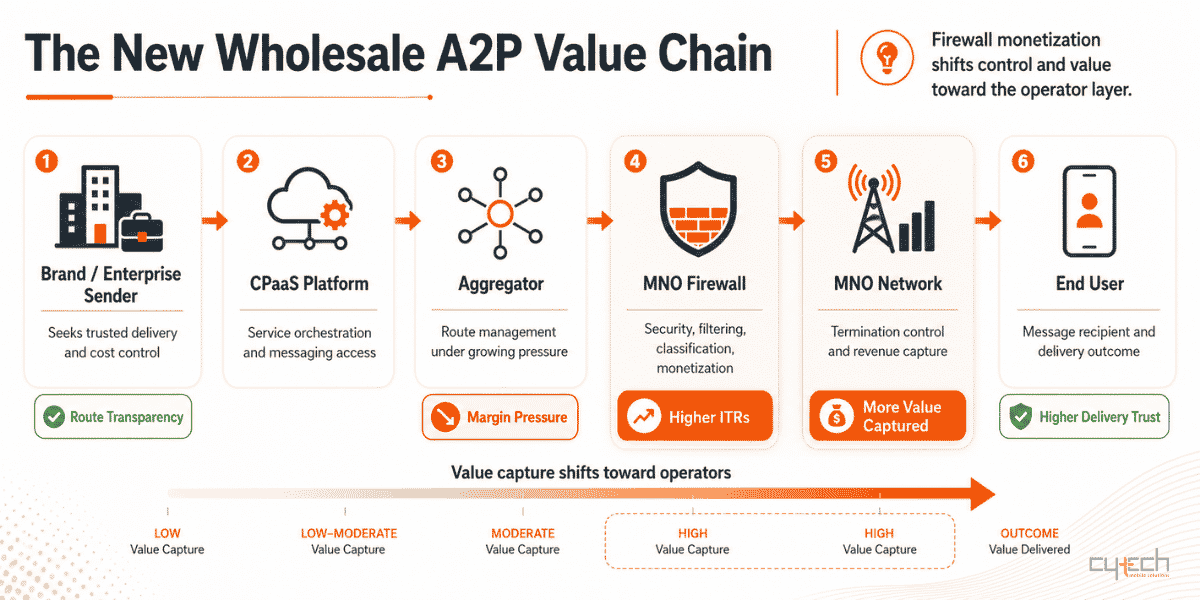

Global ITR Escalation and Aggregator Margin Compression

IfAs MNOs assert control over their networks, the traditional SMS value chain is experiencing intense financial pressure. MNOs now command the largest share of the wholesale transaction, severely compressing the margins of downstream platforms and aggregators. This pressure is best illustrated by the rising trajectory of global International Termination Rates (ITRs), which crossed the symbolic threshold of $0.10 per message for the first time in Q1 2025.

This rate increase is highly uneven. While over 107 markets remain below the global average, premium corridors in Asia and Africa feature ITRs exceeding $0.20, with select premium markets like Madagascar, Uzbekistan, Sri Lanka, and Pakistan surpassing $0.217 per message.

This pricing surge has accelerated consolidation within the cloud communications sector. For example, Proximus acquired Route Mobile for EUR 2 billion to bundle firewall functions directly into global CPaaS suites, a move that allowed consolidated players to undercut standalone firewall vendors and compress competitor margins by 15% to 20%.

The Paradox of RFP Commitments and Fraud Economics

An unintended consequence of aggressive operator monetization is the rise of Artificially Inflated Traffic (AIT), commonly known as SMS pumping. To maximize profits, many MNOs have shifted from long-term contracts to short-term, one-year exclusive partnerships. These exclusivity rights are auctioned to aggregators who must make substantial upfront financial commitments to secure the deal.

To recoup these investments, winning aggregators often hike termination rates drastically, sometimes tenfold. This extreme pricing drives legitimate enterprise buyers to exit the SMS channel in favor of cheaper alternative paths. Facing massive shortfalls in legitimate volume, contracted aggregators may turn a blind eye to—or actively collude in—AIT schemes where bots generate fake OTP requests to harvest messaging fees.

Additionally, rogue aggregators utilize “SMS trashing,” a fraud scheme identified by the Mobile Ecosystem Forum where aggregators accept messages and charge brands full price, but quietly discard them to avoid paying delivery fees to terminating MNOs.

This cleanup of the messaging ecosystem has triggered a bumpy transition. While blocking AIT has reduced the fraud economy from its 2023 peak of $2.1 billion, it has also caused a contraction in total global A2P SMS volumes, which are projected to drop from 1.9 trillion messages in 2023 to under 1.5 trillion by 2029. However, legitimate domestic white-route traffic is increasing its market share, forecast to rise from 80.6% in 2024 to 86.5% by 2029.

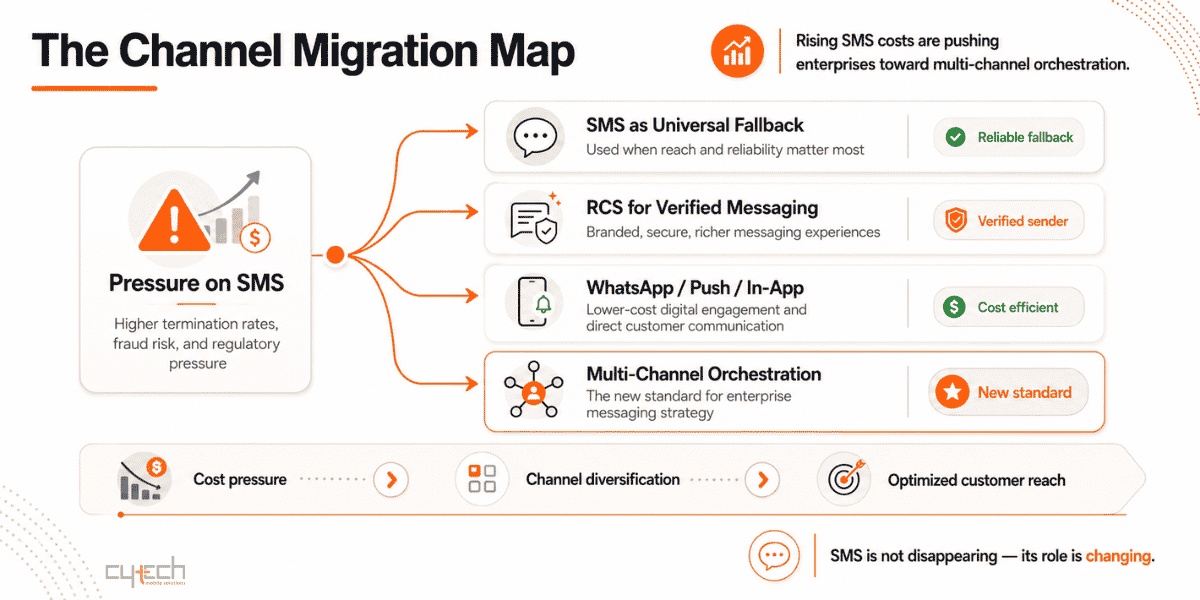

Regulatory Pushback and Channel Migration

High wholesale termination rates have also drawn regulatory scrutiny. In the United Kingdom, Ofcom identified that Mobile Communications Providers (MCPs) enjoy a position of monopoly in the termination of A2P messages. To prevent excessively high retail pricing, Ofcom proposed capping A2P SMS termination rates at an inflation-adjusted ~1.96p per message.

This regulatory intervention has faced industry pushback. Major aggregators like Sinch argue that price caps create market distortions, risk shifting costs to other free services, and ignore the reality that SMS rates are already self-regulating. Industry data shows that businesses are rapidly migrating from SMS to push notifications, WhatsApp, and in-app solutions to completely bypass expensive termination fees. For example, financial institutions and public sector agencies, such as the UK’s National Health Service, have aggressively transitioned to direct in-app notifications, shifting the bulk business messaging landscape.

The Rise of RCS and Multichannel Orchestration

Rather than completely abandoning cellular messaging, modern enterprise strategies utilize multi-channel orchestration, reserving SMS as the ultimate, universal fallback channel. Meanwhile, Rich Communication Services (RCS) is emerging as a powerful, secure alternative, heavily backed by Google and Apple’s native iOS 18 support. RCS’s conversational billing models and verified sender badges mitigate the fraud risks associated with traditional SMS.

| Message Type | Pricing Model | Delivery and Features | Typical Use Case |

|---|---|---|---|

| RCS Basic | Similar to standard SMS; billed on delivery | Verified Sender ID, up to 160 bytes of text, read receipts | One-way OTPs, secure transactional alerts |

| RCS Single | 20% to 30% higher than standard SMS | Rich media, high-res images, carousel cards, custom branding | Visual promotional campaigns, product showcases |

| RCS Conversational | Billed per 24-hour session window | Unlimited two-way messages, interactive chatbot integration | Complex customer support, conversational sales |

RCS business traffic is projected to grow 50% in 2025 alone, largely driven by iOS integration, helping operators retain business messaging traffic within traditional telecom networks.

Future Outlook

Firewall monetization has fundamentally shifted wholesale A2P economics from a volume-centric business to a trust-critical, value-centric model. Operators that leverage firewalls solely to extract high tariffs risk driving legitimate brands entirely off cellular networks. Conversely, operators and aggregators that collaborate to eliminate fraud while integrating multi-channel orchestration will build a sustainable, highly profitable business messaging ecosystem. Wholesale messaging is no longer about delivery at the lowest cost; it is about trusted completion and secure engagement.

Bibliography

- AcePeak Introduces Enterprise SMS Firewall to Help MNOs Protect A2P Revenue and Eliminate Grey Route Fraud

- How the SMS Economy Works: Aggregators, Tier 1 Carriers, and Who Pays Whom

- SMS fraud: The complete guide to detection and prevention

- SMS grey routes are expected to generate revenue leakages of US$37.1 billion between 2020-2024

- Best-in-class SMS firewall

- Best-in-class A2P Monetization

- A2P SMS News 2026: What’s Changing and What It Means for Your Business

- SMS FIREWALL MARKET SIZE & SHARE ANALYSIS – GROWTH TRENDS AND FORECAST (2026 – 2031)

- Artificially inflated traffic (AIT): Causes and solutions

- AIT – The root cause, the Solution and the Implication on RCS and Network APIs

- Business messaging: Review of the A2P SMS termination market

- Three’s response to Ofcom’s Review of the A2P SMS termination market.

- Key RCS statistics & market insights for 2026

")